For the past 21 years, my husband, Lance, has been dedicated to the same company. He started at the ground level as a contract equipment installer, and when he left, he held the position of Chief Relationship Officer. With 23.5 years of marriage under our belts, Lance's departure from the company marks a significant change for our family.

We've always known the possibility of job loss or change could happen, and have worked over the years to be prepared for that possibility. As Lance began more seriously contemplating leaving, we understood the importance of preparing ourselves for this major life transition. Big life changes—whether it's marriage, welcoming a new baby, switching careers, going through a divorce, or retiring—require careful financial planning. Here are some steps we took to prepare ourselves financially for this significant shift:

As I write this, it's only been a week since Lance bid farewell to his office and drove his final commute home. Already, the transformation is evident—he's less stressed, happier, and brimming with excitement for our future. While uncertainties still loom, we're eagerly embracing the next chapter of our lives. Our years of financial planning have laid a solid foundation, and we're ready to navigate whatever comes our way.

0 Comments

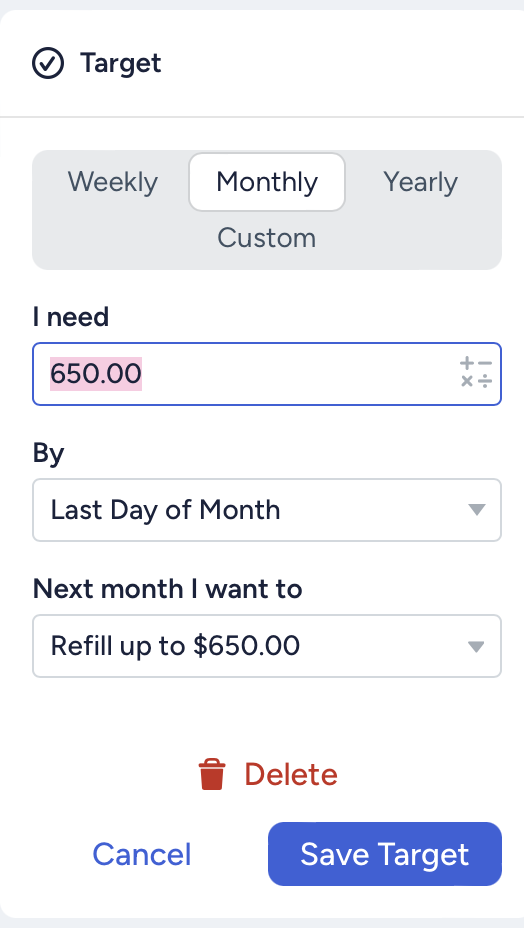

Gone are the days of puzzling over YNAB's target types! For years, we've all asked ourselves. Which target type for what expense? How to adjust for more funds? How to tailor targets so it does what I expect it to do? Now, YNAB simplifies targets. Whether you are online or mobile, just specify frequency, amount, due date, and action for the next interval. Easy, isn't it? If you haven't seen it yet, anticipate it in your budget soon! Gone are the days of puzzling over YNAB's target types! For years, they've left users scratching their heads. Which one for what expense? How to adjust for more funds? How to tailor targets? Now, YNAB simplifies targets. Just specify frequency, amount, timing, and action for the next interval. Easy, isn't it? If you haven't seen it yet, anticipate it in your budget soon! Do you want to meet to go over your targets and learn the new way of doing things? Let's set up a time to chat! Do you want to learn more about targets on your own? Check out YNAB's how-to!

While we're not typically big spenders, the no-spend month prompted us to rethink our purchases, emphasizing intentionality over impulse buys. Date Nights Initially, our date nights were more creative and elaborate, filled with planning, shopping (for a few fresh ingredients) and cooking together. I even made the table look a little more special than usual. However, as the month progressed, we found joy in simpler pleasures like homemade popcorn and ice cream. That counts as dinner, right?

Family Vacation Despite the no-spend commitment, we still enjoyed our pre-planned family Christmas vacation. It had been planned and mostly paid for months earlier. Tangent: We decided as a family a few years ago to buy less Christmas gifts and spend most of our Christmas budget on a family trip instead. Opting for quality time instead of quantity of gifts has been a nice change. Tangent over. We opted for snacks and cold cereal from the grocery store rather than eating out every meal. We chose free activities in the area and the only souvenirs we brought home were some dirt, pictures and fun memories. Kids' Perspective

When I asked my kids about the no-spend month, they expressed that it didn't feel significantly different for them. It seems they've grown accustomed to adhering to our spending plan and hearing, "not right now." Husband's Reflection My husband, who was the instigator of this little experiment had this to say, “I found myself holding back on what would otherwise be impulsive buys. It made me think about what I really needed vs wanted.” He held off on buying some high-priced tools he really wanted, but knew it wasn't the priority (I'm sure they will make their way into his shop eventually). Conclusion Reflecting on our experience, a no-spend month proved valuable in realigning our spending with our values. It's a chance to assess priorities and ensure our financial decisions enhance our lives in meaningful ways. A lot of the stress people experience with regard to finances is due to the misalignment between our spending and our values. Are we really spending with intention on those things which will enhance and improve our lives; or are we spending on things that will give us a quick thrill, but don't add much value? We plan to try this again. What are your thoughts? Would you consider embarking on a no-spend month with us the next time we give it a go?  During our yearly couples planning retreat this year, my hubby, tossed out this idea for a no-spend March. "Let's see how much we can save by giving the extras a break," he says, all hyped. He’s sure we are going to be millionaires at the end of the month by not ordering Amazon!

Four days in, folks (at the time of writing)! Together, we've put the brakes on non-essential spending. No more dining out, even on date nights – we're rocking the kitchen. Amazon quick buys? We're resisting the siren call, and our Costa Vida cravings are being set aside. Now, we don't live large, but we do have our weaknesses – hello, Costa Vida and movie downloads. Here's the scoop – we're still hitting the grocery store for planned meal ingredients, and we're keeping things like a pre-planned family getaway later this month in the plan. We're not going full hermit mode, just putting the brakes on the spur-of-the-moment non-essentials. Do you think a No-Spend Month Adventure sounds like a fun challenge for your family? Here are a few steps to prepare:

As we're just kicking off this no-spend March, we are feeling optimistic. I’ll be back next month to let you know how it went. So, who's in for a No-Spend Month Adventure? 🌟💰  Ever felt that knot in your stomach when checking your bank balance? Money isn't just about the numbers; it's a rollercoaster of emotions. Emotions wield considerable influence over our financial decisions, making it crucial to unravel the connection between our feelings and our wallets.

Understanding the psychology of money begins with acknowledging that our financial journey is deeply entwined with our emotions. Here's a brief guide on how to navigate this emotional landscape on your financial journey:

By recognizing the emotional landscape of your finances and incorporating a personalized MAP for your financial journey, you not only gain financial clarity but also foster a healthier relationship with money – one that harmonizes your emotional well-being with your financial goals. |

Heads-Up!Take a peek into my coaching journey through the years! Here, you'll see how my thoughts and wisdom have grown as I've learned from working with amazing people and expanding my knowledge Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

Proudly powered by Weebly